Does Your Business Earn Well But Still Feel Financially Tight?

A business owner in Dubai recently described it this way: “We close good deals every month. But by the 20th, we’re already watching the account.”

That feeling is more common than most people admit. And the cause is almost never low revenue. It’s the gap between when money is earned and when it actually arrives in your account.

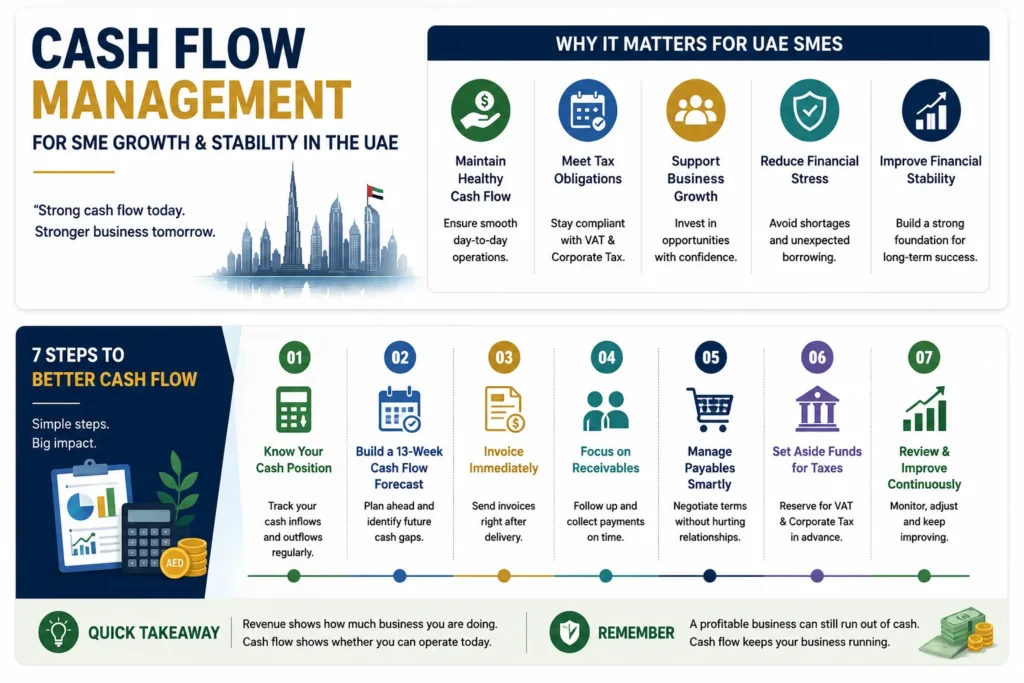

This is a cash flow problem — and for SMEs across the UAE, it’s one of the most frequent reasons a financially healthy business suddenly finds itself unable to pay suppliers, run payroll, or meet a VAT deadline.

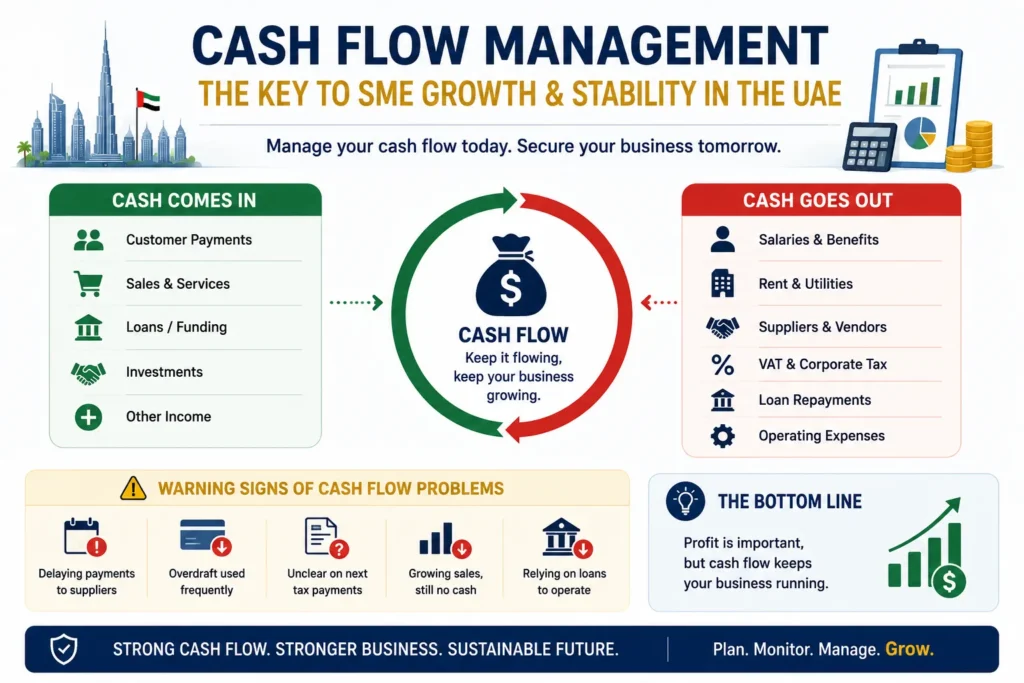

Cash flow management is the practice of monitoring and controlling how money moves through your business — so you always know what’s coming in, what’s going out, and whether you’ll have enough to cover what’s due next.

Get that right, and almost every other financial decision becomes easier.

Cash flow management is the process of tracking, planning, and controlling the money entering and leaving a business.

For UAE SMEs, it helps business owners:

- Pay employees and suppliers on time

- Meet VAT and Corporate Tax obligations

- Reduce dependence on short-term borrowing

- Plan business growth with confidence

- Avoid unexpected cash shortages

A company can be profitable and still run into financial difficulties if customer payments arrive late. This is why cash flow management is one of the most important financial practices for small and medium-sized businesses in the UAE.

Quick Takeaway: Revenue shows how much business you are doing. Cash flow shows whether you can comfortably operate the business today.

What Is Cash Flow Management? (Definition for UAE SMEs)

The Basic Concept

Cash flow is the movement of money into and out of your business over a given period of time.

Money flows IN through:

- Customer and client payments

- Product sales and service contracts

- Business loans or investor funding

- Asset sales or other income

Money flows OUT through:

- Employee salaries and benefits

- Office or warehouse rent

- Supplier and vendor invoices

- VAT and Corporate Tax payments to the FTA

- Software, utilities, and daily operating costs

- Loan repayments

Cash flow management is the active process of tracking, forecasting, and controlling that movement so your business never runs out of cash at the wrong moment.

Cash Flow vs Profit: Why They Are Different

This is one of the most misunderstood areas of business finance — and one of the most consequential.

Here’s a real-world example.

A trading company in Dubai completes AED 600,000 in orders during Q1. Margins are healthy. The income statement shows a profit. But the clients are on 60-day payment terms. Meanwhile, staff salaries, rent, and supplier invoices all fall due within two weeks.

On paper: profitable. In the account: not enough cash to meet obligations.

Profit is what remains after subtracting costs from revenue — it’s an accounting figure.

Cash flow is the actual money available in your business at any given moment.

A business can be profitable and still fail if it consistently runs out of cash.

A Real Example from a UAE Trading Business

Imagine a trading company in Dubai that secures AED 800,000 worth of sales during a quarter.

At first glance, everything looks positive. Sales targets have been achieved and profit margins appear healthy.

However, most customers are on 60-day payment terms.

While waiting for those payments, the business still needs to cover:

- Employee salaries

- Warehouse rent

- Logistics costs

- Supplier invoices

- VAT obligations

Even though the company is profitable on paper, cash may become tight before customer payments arrive.

This situation is one of the most common reasons growing businesses experience financial pressure despite strong sales performance.

The lesson: Profit measures performance. Cash flow determines whether obligations can be paid on time.

Key Statistic: Inaccurate cash flow forecasting is linked to 82% of SME business failures in the region, according to UAE financial research (TaxNews.ae, 2026). The vast majority of those failures were preventable with earlier planning and better financial visibility.

Why Cash Flow Pressure Is Higher for UAE SMEs

Running an SME in the UAE comes with specific financial obligations that directly affect your cash position — beyond what most SMEs in other markets face.

VAT and Corporate Tax Create Fixed, Non-Negotiable Deadlines

Since VAT was introduced in 2018 and Corporate Tax in 2023, UAE businesses carry structured quarterly and annual payment obligations to the Federal Tax Authority (FTA). These deadlines don’t move.

If VAT collected on sales hasn’t been held separately, the quarterly filing becomes a sudden cash drain. Corporate Tax — charged at 9% on taxable profits above AED 375,000 — needs monthly provisioning throughout the year to avoid a year-end shock.

Long Client Payment Terms Create Cash Gaps

In the UAE, 30 to 90-day payment terms are standard across construction, logistics, trading, and professional services. That means completing work in January but receiving payment in March — while February expenses don’t pause.

Business Growth Itself Creates Short-Term Cash Pressure

Taking on larger contracts, hiring new staff, or moving to a bigger office all require upfront spending before the additional revenue arrives. Without a plan, periods of growth can temporarily leave a business more financially exposed than before.

Why Growth Can Sometimes Create Financial Stress

Many business owners assume cash flow problems only happen when sales decline.

In reality, growth can create similar challenges.

Consider a marketing agency in Abu Dhabi that wins several new client contracts within a short period.

To deliver the work, the agency hires additional staff, invests in software subscriptions, and increases advertising spend.

The costs begin immediately.

Client payments, however, may not arrive for another 30 to 60 days.

The business is growing successfully, yet cash flow becomes tighter than before.

This is why growing companies often need stronger cash flow planning than businesses that remain the same size year after year.

[H3] SME Credit Access Remains Limited

SMEs across the Middle East and North Africa receive just 8% of total bank credit, compared to 22% in high-income economies globally (World Bank / International Banker, 2025). When external financing is difficult to access, your own cash reserves become your primary protection.

Warning Signs: Is Your Business Cash Flow at Risk?

Cash flow problems rarely appear overnight. They build slowly through habits and patterns that seem minor individually but compound over time.

Warning Sign | What It Suggests |

You regularly delay paying suppliers | Cash is running low before month-end |

Overdraft is used every single month | No real cash buffer exists |

You don’t know your next VAT deadline | No financial forecasting in place |

Revenue is growing but cash still feels tight | Collections not keeping pace with growth |

Personal and business finances are mixed | No real visibility into business cash position |

You make spending decisions using only the bank balance | Unaware of upcoming obligations |

If two or more of these apply to your business, your cash flow system needs attention before a larger problem develops.

How to Manage Cash Flow in a Business: 7 Practical Steps for UAE SMEs

Effective cash flow management for small business doesn’t require a finance team or enterprise software. It requires consistent habits and a clear picture of where the money stands at all times.

Step 1 — Know Your Monthly Cash Position

Every month, before the month begins, write down:

- All expected incoming payments: which clients, how much, when

- All outgoing obligations: salaries, rent, suppliers, VAT, loan repayments

- The difference between the two — your net cash position

If the result is negative, you have time to act. If you only check this after the month has started, your options are already limited.

Step 2 — Build a 13-Week Rolling Cash Flow Forecast

A rolling 13-week forecast is one of the most practical cash flow management tips available to any UAE business. It covers roughly three months ahead — far enough to see problems forming and close enough to be accurate.

Review and update it every week. When a client confirms a payment or a supplier sends an invoice, your forecast should reflect it immediately.

Benchmark: Healthy UAE SMEs typically maintain a 25% cash-to-sales ratio before major tax periods (TaxNews.ae, 2026). Use this as a reference point when assessing your own position.

Step 3 — Invoice Immediately After Every Delivery

Every day you delay sending an invoice is a day the payment cycle gets pushed back. Invoice the same day work is completed or a product is delivered. Include clear payment terms on every invoice — 14 or 30 days, stated explicitly.

For repeat clients, consider automated invoicing through accounting software to remove the delay entirely.

Step 4 — Follow Up on Receivables Every Week

Most businesses chase overdue invoices only when cash becomes tight — by which point the pressure is already on.

Instead, review your outstanding receivables weekly and follow up at day 15, not day 45. For clients with a history of late payments, consider requiring a partial upfront payment before work begins.

Step 5 — Use Your Supplier Payment Terms Fully

Pay invoices on the final day the terms allow — not before, unless an early payment discount is offered. Holding cash in your account for the full payment period gives you flexibility for near-term needs.

This is a small but effective piece of business cash flow management that costs nothing to implement.

Step 6 — Separate Business and Personal Finances

This is one of the most common mistakes among UAE startup founders and owner-managed SMEs. When personal and business money are mixed, there is no reliable way to see your true cash position.

Open a dedicated business bank account. Keep every transaction separate from day one.

Step 7 — Build and Protect a Cash Reserve

Work towards holding at least two to three months of total operating expenses in a separate reserve account.

If your monthly running costs are AED 100,000, your target reserve should be AED 200,000 to AED 300,000. This buffer protects you when a large payment is delayed, a seasonal slowdown hits, or an unexpected cost appears.

Important Mistake to Avoid

Many UAE business owners check their bank balance and use that single number to make spending decisions. But your balance today doesn’t show the VAT filing due in ten days, the payroll run at month-end, or the three supplier invoices already approved and pending. Always check your full cash flow picture — not just your current balance.

Five Long-Term Benefits of Strong Cash Flow Management

Good small business cash management isn’t just about avoiding problems. Done consistently, it becomes an active advantage.

1. Operations Run Without Disruption

When cash is predictable, obligations get met on time — salaries, rent, suppliers, and tax payments. That reliability protects your team, your supplier relationships, and your reputation.

2. Growth Decisions Become Clearer and Less Risky

Expansion requires spending money before new revenue arrives. When you know your cash position clearly, you can make hiring, investment, and contract decisions based on real numbers — not assumptions or best-case hopes.

3. You Build Resilience for Unexpected Events

Every business faces surprises — a major client delays payment, a project runs over, equipment needs urgent repair. Businesses with healthy cash reserves respond to these situations. Businesses without them get destabilised by them.

4. Supplier Relationships Strengthen

Suppliers remember the businesses that pay reliably. Consistent payment often earns better terms, priority service, and goodwill — all of which feed directly back into your own operations.

5. Dependence on Emergency Borrowing Decreases

Short-term loans and overdraft facilities carry interest costs. Businesses that rely on them repeatedly to fill recurring cash gaps end up paying significantly more over time. Stronger cash flow management reduces that reliance.

How Accurate Bookkeeping Supports Cash Flow Management

You cannot plan what you cannot see. Accurate, up-to-date financial records give you the visibility to manage cash flow with confidence.

When your accounting and bookkeeping is current, you know exactly:

- Which clients owe you money and by when

- Which supplier invoices are due in the next 30 days

- What your actual monthly operating costs are

- How much VAT and Corporate Tax you owe to the FTA

Without that foundation, any cash flow forecast you build is guesswork. With it, your planning is grounded in real data.

Many UAE SME owners stay focused on operations while financial records quietly fall behind. By the time they review the books, decisions from the previous weeks were made on incomplete or inaccurate information. Keeping records current is one of the highest-value activities a business owner can prioritise.

A Simple Example of How Bookkeeping Improves Cash Flow Visibility

Let’s assume a Sharjah-based service company believes it has AED 250,000 available in its bank account.

At first glance, the balance looks healthy.

However, after reviewing its financial records, management discovers:

- AED 45,000 in supplier payments due next week

- AED 60,000 in payroll obligations

- AED 18,000 in VAT payable

- AED 22,000 in recurring operating expenses

Suddenly, the available cash position looks very different.

Without accurate bookkeeping and reporting, these obligations can easily be overlooked until they become urgent.

This is why reliable financial records are not just an accounting requirement. They are a decision-making tool.

Tools That Help with Small Business Cash Management in the UAE

Several accounting platforms are widely used by Dubai and UAE SMEs for real-time cash tracking and VAT reporting:

- Xero — popular with professional services and consulting firms

- QuickBooks Online — widely used by trading and retail businesses

- Zoho Books — FTA-approved, cost-effective for growing SMEs

- Sage Business Cloud — suited for businesses with more complex inventory needs

Each of these integrates with UAE VAT requirements and makes FTA filing significantly more straightforward.

VAT, Corporate Tax, and Cash Flow: Planning Together Prevents Crises

VAT Cash Flow Planning

If you’re VAT-registered, you collect 5% on every taxable sale. That amount belongs to the FTA — it was never yours to use for operations. Every month, set that portion aside in a separate account so the quarterly filing doesn’t create a sudden shortfall.

Corporate Tax Cash Flow Planning

At 9% on taxable profits above AED 375,000, the annual Corporate Tax bill can be significant. Rather than facing it as a lump sum at year-end, set aside a monthly provision based on your projected profits.

If you’re unsure how to structure tax provisioning alongside your cash plan, our Tax Consultancy team works with UAE SMEs to plan these obligations in advance — so tax season never becomes a cash emergency.

When to Bring in a Financial Consultant for Cash Flow Support

If cash flow is consistently tight despite reasonable revenue, the issue is rarely the volume of sales. It’s usually in how money is tracked, collected, or planned.

A qualified financial consultant can:

- Build a cash flow tracking and forecasting system specific to your business

- Identify where collections are slow or expenses are uncontrolled

- Create a 12-month cash flow plan aligned with your UAE tax calendar

- Prepare your financial records for VAT filings and FTA reviews

- Review your books ahead of any audit or regulatory examination

At Expert Edge UAE, our Chartered Accountants and financial consultants have over 15 years of experience supporting SMEs across Dubai, Abu Dhabi, Sharjah, and the wider Emirates. We also offer Audit Services to make sure your records are accurate and defensible before any formal review.

Conclusion: Cash Flow Is the Foundation of a Stable UAE Business

Revenue shows you how much business you’re doing. Profit shows you the margin. But cash flow shows you whether the business can actually keep operating — through slow months, growth phases, tax seasons, and the unexpected.

For UAE SMEs managing VAT deadlines, Corporate Tax obligations, supplier relationships, and long client payment cycles all at once, clear and consistent cash flow visibility isn’t a nice-to-have. It’s the foundation that everything else is built on.

The businesses that track this well are the ones that can hire with confidence, take on bigger contracts, handle surprises without panic, and build something that lasts.

If your business needs support with accounting, cash flow planning, VAT compliance, or financial reporting, the team at Expert Edge UAE is ready to help.

Frequently Asked Questions About Cash Flow Management for UAE SMEs

1. What is cash flow management in simple terms?

Cash flow management means keeping close track of how money enters and leaves your business. The goal is to make sure enough actual cash is available at the right times to pay staff, suppliers, rent, and taxes — even when some clients are slow to pay.

2. Why do profitable UAE businesses still run into cash problems?

Because profit is recognised when a sale is made, but cash only arrives when a client actually pays. If your clients are on 60 or 90-day payment terms, you can show a healthy profit figure while having very little cash available today. Managing that timing gap is what cash flow management is designed to address.

3. What are the best cash flow management tips for small businesses in Dubai?

Invoice clients immediately after delivery. Follow up on outstanding payments every week. Set aside VAT and Corporate Tax provisions monthly. Hold a cash reserve of two to three months of expenses. Separate business and personal accounts. Build a 13-week rolling forecast and review it weekly.

4. How does Corporate Tax affect cash flow for UAE businesses?

Corporate Tax is 9% on taxable profits above AED 375,000. If you haven’t been provisioning for this throughout the year, the annual payment arrives as a large, unexpected drain. Planning for it monthly — as a fixed percentage of profits — prevents it from becoming a cash crisis at year-end.

5. How much cash reserve should a UAE SME hold?

The practical target is two to three months of total operating expenses. If your monthly costs are AED 80,000, aim to hold between AED 160,000 and AED 240,000 in reserve. This covers delayed receivables, seasonal slowdowns, and unplanned costs.

6. What is invoice financing and when should UAE SMEs use it?

Invoice financing allows you to borrow against outstanding invoices before your clients pay. It’s a useful short-term bridge when a large receivable is delayed and near-term obligations are due. It’s a tool for managing timing gaps — not a substitute for stronger collections or better payment terms.

7. How does bookkeeping connect to cash flow management?

Accurate bookkeeping gives you real-time visibility into what clients owe you, what you owe suppliers, and what’s coming up in the next 30 to 60 days. Without current records, every cash flow forecast is built on incomplete information — and that leads to surprises.

8. When should a UAE SME work with a financial consultant on cash flow?

If you’re regularly surprised by cash shortages, struggling to meet VAT or Corporate Tax deadlines, or making growth decisions without clear financial numbers, professional support adds immediate value. The earlier proper financial systems are in place, the less disruptive the transition is.